“A man who pays his bills on time is soon forgotten”

– Oscar Wilde

Unlike some of his predecessors, the eccentric Wilde never landed himself in debtors’ prison. He certainly paid his dues in time to avoid following in the footsteps of Robinson Crusoe and Daniel Defoe, but he is anything but forgotten and often regarded as one of the leading (if not controversial) playwrights and novelists of his era. His words, however, shouldn’t be taken literally; they imply that a person who pays their debts on time is left undisturbed by their creditors.

Since the abolition of these archaic English penitentiaries in 1869, some may think that the risks of loan delinquency have been sidelined as well. In truth, they have, as all things do, simply evolved with the times. The question is: what exactly have they become?

What is a Credit Score?

In a nutshell, your credit score is a metric that estimates your likelihood to pay your debts on time. This three-digit number, ranging from 300 to 900, is representative of your creditworthiness and how well you manage credit in general.

In an inverse relationship, lower scores indicate to lenders that you are a higher-risk investment. At the end of the day, the private and public lending sectors are investing (lending) in a product (you) with the intention of realizing a return (the principal amount plus interest) in the future. Conversely, a higher score signals that you are likely to make your creditors whole.

At the end of the day, your credit score is a tool that lenders use to better manage their risk and hopefully guarantee a return on their investment.

How Are Credit Scores Calculated?

The processes in place are more complex than we’ll get into today, but generally speaking, they are a holistic reflection of your credit history. Most people are familiar with the usual suspects: how often you made payments on time, how much was owed, and how often you were late on payments.

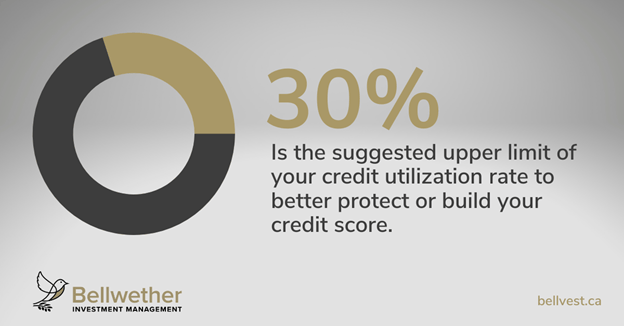

A less commonly understood aspect that factors into the equation is the debt-to-credit ratio, otherwise known as your credit utilization rate. In essence, it is a function of how much revolving credit (credit cards or lines of credit, for example) is being used divided by the total amount of credit issued to you. If you have a credit limit of $50,000 and had $10,000 in revolving debt, your debt-to-credit ratio would be 20%. As far as credit scores go, a useful target ratio is anything below 30%. Anything north of that figure may communicate to lenders that you may face difficulties when trying to pay back your loan.

How Are Credit Scores Used?

As alluded to, credit scores are one of the primary factors that help companies determine loan approval. With higher scores, you can qualify for better borrowing terms, higher limits, and lower interest rates, whereas lower scores may experience the opposite of these benefits.

The FICO score, developed by the Fair Isaac Corporation, is the most common measurement used by financial institutions. The data used to determine that three-digit number standing between you and a mortgage are as follows:

- 35% payment history

- As the most heavily weighed category, lenders want to know how diligently you made your payments and if they were on time.

- 30% amounts owed

- This largely accounts for the debt utilization rate mentioned previously, and if you are overextended or using a large portion of your total limit, it may lower your score.

- 15% length of credit history

- To better understand your track record, lenders check to see how long your accounts have been open (including the oldest, youngest, and average age if you have multiple accounts) as well as how long it has been since they’ve last been used.

- 10% new credit

- According to research, opening multiple new credit accounts in quick succession shows greater risk as it indicates potential financial pressures.

- 10% credit mix

- If you have a mix of different forms of credit (revolving accounts such as credit cards and installment accounts such as auto loans), it shows a level of credit management competency.

It is important to know that your credit score only reflects the information held within your credit report itself. Lenders look at other factors to dictate the risk levels of each loan they issue, which can include age, length of employment, and income. Compared to an elderly individual who has no stable income, a young professional making a six-figure salary will, in all likelihood, be more likely to pay their lenders back.

How Can I Improve My Credit Score?

The basics are known by most Canadians: pay your minimum (if not more) balances on time, use your existing credit sparingly, keep building a track record by aging your accounts, limit your hard credit checks, and improve your credit mix.

There are different methods as well that range in their complexity. One tactic is to increase your credit limit. At first glance, this may seem off-colour, but doing so can improve your debt-to-credit ratio so long as you increase your limit and not your spending. If you find yourself drowning in debt, we’ve written an article on debt reduction strategies, which you can read here.

What is more important is managing your debt and creating a financial plan to keep your credit accounts in line. Thankfully, Bellwether Family Wealth Advisors specialize in exactly that. They can help you strike the right balance between having access to credit and how to best use it for your own sake.

Building credit takes time, but in the long run, it can save you a tidy sum on interest fees. It’s better to start sooner rather than later, but later is still better than never.

Next Previous