“You don't build a business. You bild people, and people build the business."

– Zig Ziglar

Having given countless motivational speeches and even trained the likes of Will Harris, a bestseller and international speaker in his own right, Ziglar knew how to build people up. As the prolific American author did so, the people built the foundation for successful businesses themselves.

With the addition of Employee Ownership Trusts (EOTs) introduced in Budget 2023, will Canadian small business owners achieve the same? Or will the qualifying conditions and tax benefits limit EOTs as a viable succession planning tool?

The Landscape for Canadian Small Business Owners

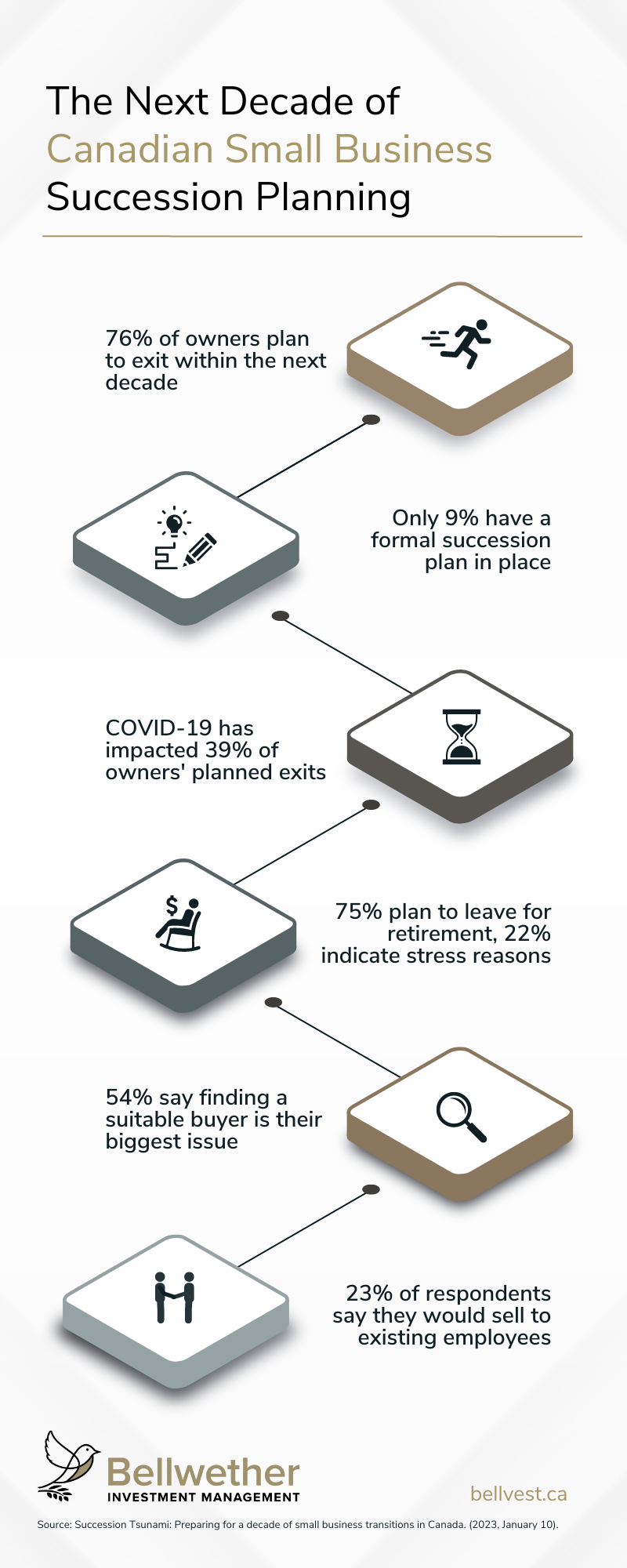

In a 2023 report from the Canadian Federation of Independent Business (CFIB), named Succession Tsunami, it’s made clear that a tidal wave of businesses changing hands will hit the economy sooner rather than later. To name a few key statistics:

To bring it all together, over $2 trillion in business assets are set to change hands over the next decade. To put that into perspective, that’s larger than Spain’s 2021 gross domestic product (GDP), according to the World Bank, but less than one tenth of business owners have an established succession plan to ease these transactions along smoothly.

What Is An Employee Ownership Trust?

In its most simple terms, Canadian business owners now have a new option for succession planning. Coming into force on January 1, 2024, EOTs allow employees to become partial owners of their workplaces by purchasing the business over time.

Research suggests that employee-owned businesses grow at faster rates, are more resilient to failure, and tend to be more productive than ones with concentrated ownership structures. From a business perspective, it seems beneficial. On a human level, the data points toward increased employee retention, benefits, retirement savings, and a slew of other benefits.

How to Qualify as an Employee Ownership Trust

The criteria necessary to form an EOT are as follows:

- Must be a Canadian resident trust, excluding deemed resident trusts.

- Holds shares of qualifying businesses for the benefit of the employee beneficiaries of the trust itself.

- Make reasonable distributions to employee beneficiaries under a formula that only considers an employee’s length of employment, remuneration, and hours worked. If distributions are not made under such considerations, all employees must be treated similarly.

- Similarly, an EOT is prohibited from allocating shares of a qualifying business to individual beneficiaries.

- The EOT must retain a controlling interest in the shares of one or more qualifying businesses.

- All, or substantially all, of the EOT’s assets must be shares of qualifying businesses.

To be considered a qualifying business, it must:

- Be a private Canadian corporation where all, or substantially all, of the fair market value of its assets is attributable to assets used in actively conducting business in Canada.

- Not carry on business as a partner in an existing partnership.

EOT beneficiaries consist exclusively of qualifying employees. This includes any individual employed by the qualifying business except for:

- Employees or their related persons with a significant economic interest in the qualifying business.

- Employees that have not completed a probationary period of up to 12 months.

- Employees that are 18 years of age or younger.

What Are the Tax Benefits of Employee Ownership Trusts?

There are a few key features that will provide relief to both owners and employees. Unlike most trusts, EOTs will be exempt from the 21-year deemed disposition rule that requires trusts to dispose of their property after their time is up.

By putting an expiration date on trusts, it effectively prohibits one from deferring capital gains taxes indefinitely. While it limits certain people trying to game the system from one generation to the next, it makes less sense in the case of EOTs. Shares in the qualifying company can be held indefinitely for the benefit of the employees.

For owners transferring qualifying businesses to an EOT, the capital gains reserve period will be extended to 10 years. The change requires that a minimum 10% of the deferred gain must be brought into income annually. This should allow for more greater tax flexibility, compared to the standard five-year period.

Finally, the one-year repayment requirement of shareholder loans is undergoing renovations as well. EOTs will be able to borrow funds from the qualifying business itself and will not face tax consequences if paid back within a 15-year period.

What's Missing From Employee Ownership Trusts?

Uptake may be slower than assumed under the current proposed rules. The tax benefits, although a step in the right direction, leave something to be desired.

The capital gains reserve, for example, only serves the business owner if they choose to get paid out over several years instead of in a lump sum. For many, the value of their wealth is on paper within the business itself, and the sale of the company was most likely a key piece of their retirement. In 2014, the U.K. exempted capital gains taxes from owners selling a controlling interest to EOTs, which saw employees become owners at shocking rates.

While the other two proposed changes (loan repayment and deemed disposition) are certainly beneficial, they do not change the fact that EOTs will be typically taxed as inter vivos trusts at the peak marginal tax rate. Distributions to beneficiaries, however, will be taxed at their personal rate, and dividends can maintain their eligibility for tax credits.

With the government’s fiscal impact projections weighing in at $20 million in revenue loss over 5 years, it seems they do not forecast mass adoption of EOTs either.

What Are the Benefits of Employee Ownership Trusts?

It may not be about financial incentives after all. For business owners providing a niche product or service, finding a buyer may be more difficult than anticipated. For entrepreneurs with no clear successors or uninterested next of kin, employees may be the closest they have to family. For founders who want to slowly ease their way out of the day-to-day, this can help them do so.

Canadian EOTs are not as financially enticing as similar structures seen in the United States or the United Kingdom. But more importantly, they are not punitive to owners hoping to close the gap on wealth disparity and help employees reap the rewards of partnership. It might be helpful to view EOTs as a commercial incentive, not a tax break.

EOTs are certainly not a one-size-fits-all solution, and it is vital that Canadian business owners speak with financial professionals to find the best path forward. But leaving your business behind and heading into retirement is about more than just the sale. It’s about fulfillment, leaving a legacy, and preserving the work culture you created over decades.

At Bellwether, our Family Wealth Advisors can help with all of that and more.