“Housing affordability is a significant problem in Canada—but not one that can be fixed by raising or lowering interest rates.”

— Tiff Macklem, Governor of the Bank of Canada

The Bank of Canada’s Governing Council, those responsible for setting monetary policy, recently deliberated over how to best handle interest rates going forward. While many of their key indicators are on course for hitting their inflation targets, some have proven… more difficult to manage.

Understanding the Consumer Price Index (CPI)

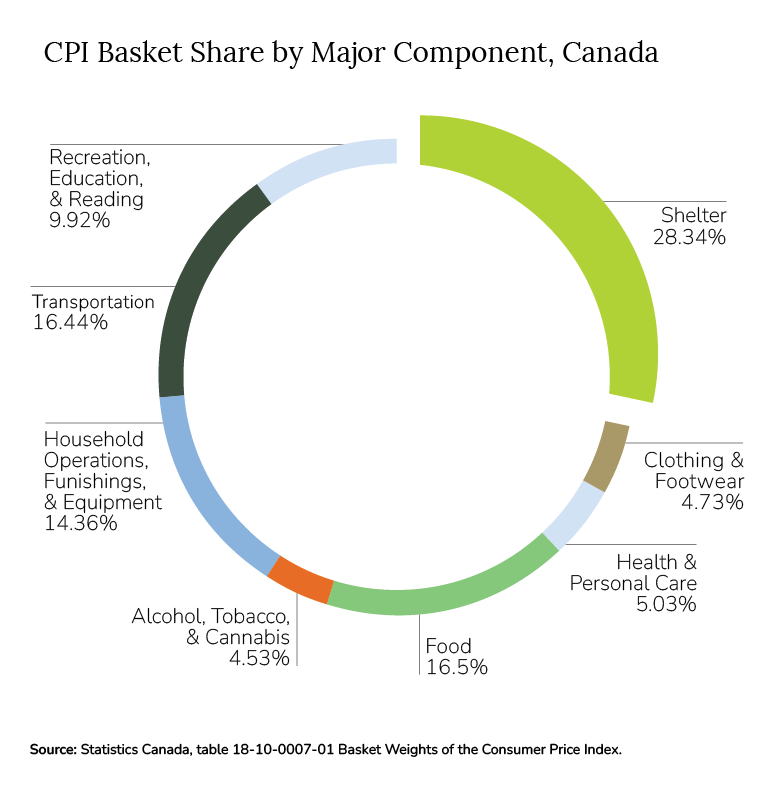

The CPI measures changes in prices for the average Canadian consumer by calculating the price changes of eight “fixed baskets of goods and services” over time.

According to data released by Statistics Canada in late February, annual CPI inflation actually fell to 2.8%, which continued the downward trend from 2.9% in January. For the first time since early 2021, inflation has met the BoC’s target range of 1% to 3% for two consecutive months.

While consumers paid less for sneakers and seafood, shelter inflation remains high, at a lofty 6.5% on a year-over-year basis. Breaking that down further, rent climbed by 7.8%, and mortgage interest costs rose by a staggering 27.4%, placing upward pressure on inflation.

As pointed out by TD, shelter inflation accounts for more than half of overall inflation. With mortgage resets on the horizon, some Canadian homeowners may be straddled with monthly payments increasing by thousands of dollars, further exacerbating shelter’s oversized impact on the BoC’s preferred measurement for setting monetary policy.

So why not just cut interest rates and save mortgagors—and everyone struggling with rising costs—the hassle?

The Double Bind

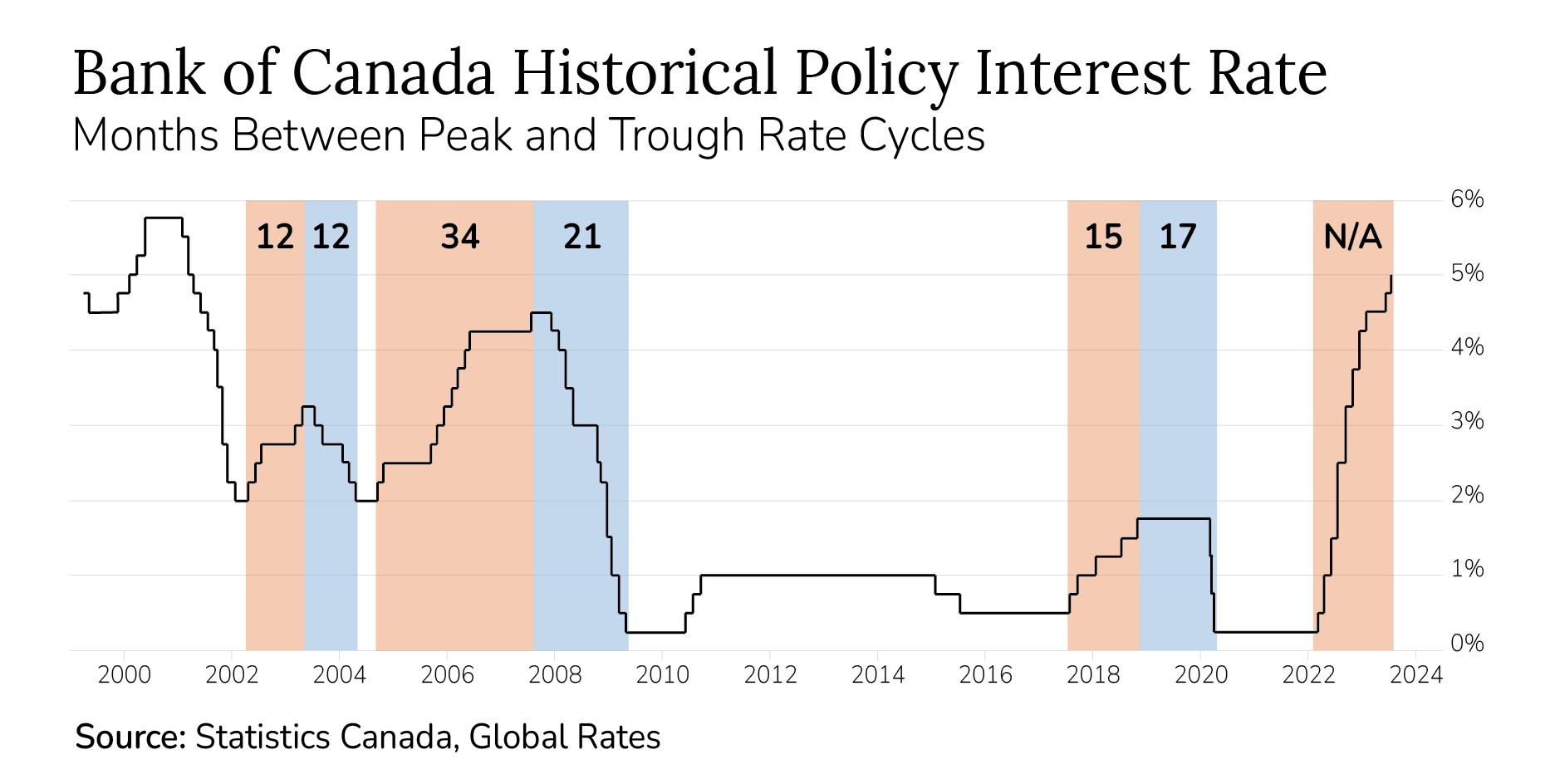

Although BoC officials believe interest rate cuts are likely within the next year if the economy stays on track, there is some disagreement on the exact timeline and associated risks.

Investors responded favourably to the message (alongside a similar Fed announcement of anticipated rate cuts this year), sending the S&P/TSX composite index up by 185.13 basis points by market close on March 20th, 2024.

But the Governing Council must wrestle with cause-and-effect. As stated by the BoC, if “the housing sector rebounds in spring, shelter price inflation could be pushed up” and effectively delay how quickly we reach our 2% target, or even undo their current progress.

The spring and fall seasons typically see a peak in housing demand, as timely inventory replenishments meet the renewed interest for both resale and new homes. High interest rates have dampened the shared excitement buyers and sellers generally feel this time of year.

Any sign of lowering interest rates will likely improve buyers’ demand and developers’ willingness to release inventory. The current environment, however, has caused homeowners to stay put and developers to stand pat.

And this is the key problem: sidelined would-be buyers may show interest in an instant, but new housing projects would take years to complete, further pressuring an existing supply crunch. Although slashing interest rates will soften mortgage payments—itself a massive inflationary pressure—it would likely push up sale prices and, as a consequence, the CPI.

Remember 2016?

Inflation metrics are being held up by shelter’s outsized impact, and several Canadian banks have considered what the outcome would be if it were removed from CPI measurements. It’s not unheard of, as the BoC excluded mortgage interest costs from its CPIX preferred inflation reading in 2016.

Douglas Porter, chief economist at BMO, points out that “if you take out mortgage interest costs alone, inflation is basically at 2% on the button.” James Orlando, director and senior economist at TD, shows that if Canada used “the Fed’s preferred method … inflation would be at just 2.1%” year-over-year. In a paper released in January of this year, TD’s projections suggest that in order to sustain the BoC’s 2% target, all other baskets would have to decelerate to around 0.5% to offset rising housing costs.

Don't Bank On It

If you’re hoping that the BoC will ignore shelter when setting monetary policy, you may be disappointed. First, Statistics Canada dictates CPI calculation components. Second, housing is a real, significant expense for citizens. Third, and most importantly, rate cuts don’t happen overnight.

As mentioned earlier, the hint of incoming rate cuts could bring new interest to the market for the long-term outlook. The tangible effects, however, aren’t as sudden—monetary policy can take years to unwind through measured, incremental interest rate reductions.

We may or may not be at peak interest rates, but assuming we are, the trail back down is likely to be a long one.

Carve Your Own Path

Looking towards the future is vital for portfolio management, but hopeful thinking or trying to imagine a world where shelter is not factored into CPI and monetary policy isn’t very productive.

Our outlook is simple: control what you can. While central banks work at bringing the cost of living back into line without damaging the economy through overly harsh monetary policy, we’ll take advantage of the opportunities it presents.

Participating in infrastructural projects is often reserved for institutional investors, but those with access can reliably diversify their portfolio. In comparison to residential real estate in a complicated high-interest rate environment, this reliability stands out as a key feature:

-

Inflation Protection: Contractual agreements with built-in inflation protections can insulate portfolios from unfavourable economic conditions.

-

Best of Both: Combining the potential of long-term capital appreciation with predictable, regular income generation.

-

Always Needed: As essentials for a functioning society, infrastructural projects exhibit lower sensitivity to business cycles.

-

Stability: Private investments have a lower correlation to public market fluctuations, providing stability to portfolios.

Most people can’t easily realize these benefits to shelter against elements outside of their control—inflation, central bank policies, the list goes on. With this in mind, we created the Bellwether Real Estate & Infrastructure Fund to solve two problems and ask one very important question.

-

Few households meet the criteria to access these investment opportunities, but every single one of our clients can do so through us.

-

The minimum investment requirements are significant, typically requiring years of commitment. Our fund offers our clients weekly liquidity as needed.

-

If the everyday family can’t access the same investment opportunities as some of the largest global financial institutions, how can they get ahead and build long-term wealth?