“A stock dividend is something tangible—it’s not an earnings projection; it’s something solid, in hand. A stock dividend is a true return on the investment. Everything else is hope and speculation.”

— Richard Russell

Earning money is great, but keeping it is even better. Any well-constructed portfolio will plan to optimize after-tax returns through a variety of mechanisms, and dividend income can be especially useful once you understand how the tax credit system works.

What are dividends?

Companies with excess capital can decide to sit on a war chest of capital, reinvest in their operations, or distribute earnings to shareholders in the form of a dividend.

The latter is common for established companies—if they’ve reached maturity, it’s likely that they’ve already invested in becoming an efficient, stable business, and paying dividends both rewards existing shareholders and entices prospective ones.

What are dividends?

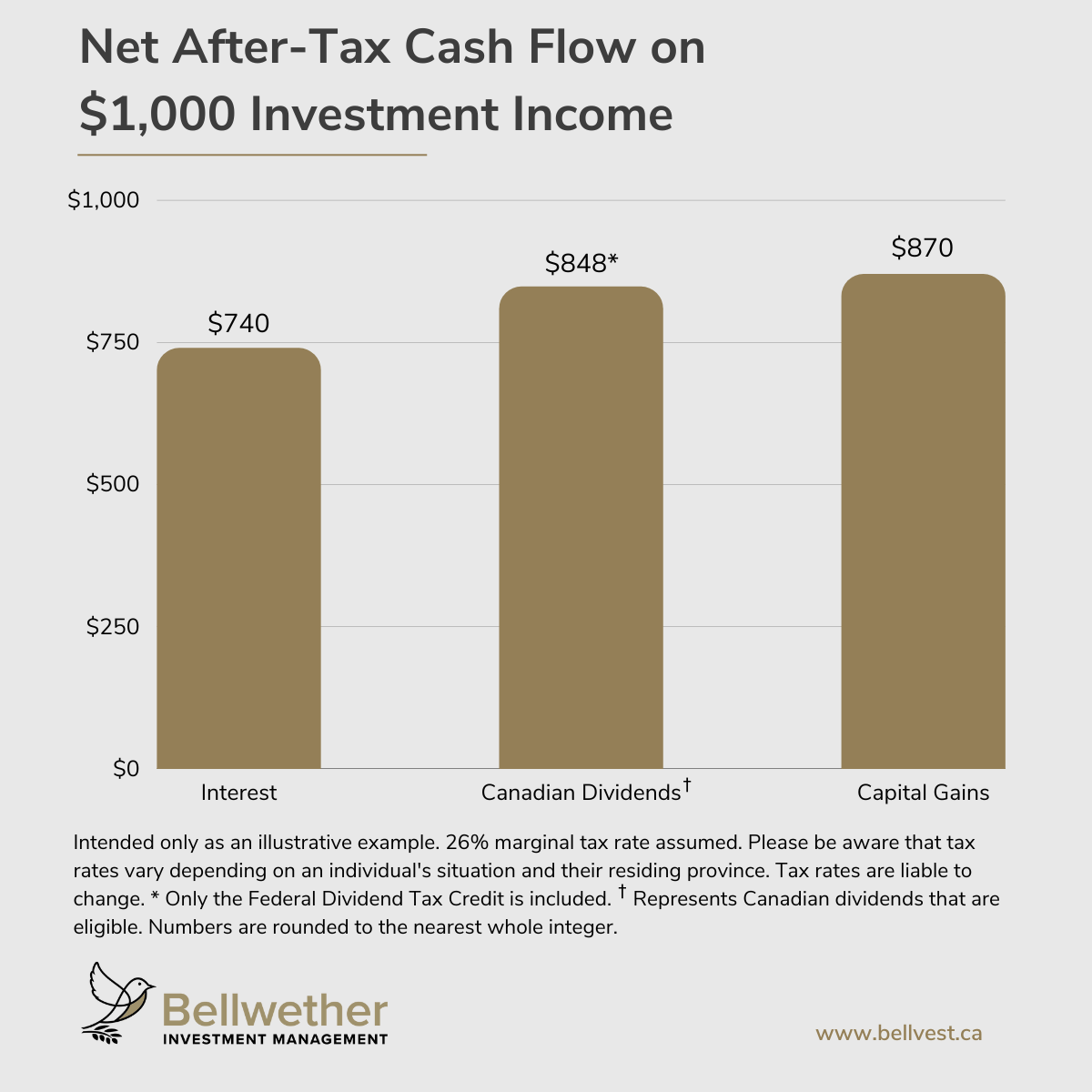

While today’s topic is focused on dividends specifically (and because we’ve already published an article regarding tax-efficient investing), here’s a brief overview of how different forms of income are taxed accordingly.

We can categorize income into three broad categories. As seen above, capital gains yield an optimal after-tax outcome, interest income takes quite a toll, and Canadian dividends land somewhere in the middle.

So, why even discuss dividends if capital gains are taxed more favourably? Barring the proposed changes to capital gains inclusion rates, non-dividend-paying equities present only one opportunity to generate returns—selling the underlying asset.

Shares in dividend-paying companies have the same opportunity, allowing investors to benefit from potential appreciation. The difference is that they get paid while they wait for the eventual sale.

Both the point of sale and the dividends themselves are tax-efficient forms of income.

How Are Dividends Taxed in Canada?

How dividends are taxed varies. Like all forms of income, it depends on your marginal tax rate and provincial laws. The differentiating factor for dividends, however, depends on whether they’re eligible or noneligible, their “gross up” rate, and the dividend tax credit (DTC).

What Are Eligible Dividends?

Large, publicly traded Canadian corporations that don’t qualify for the small business tax deduction can pay dividends to shareholders from business income that has already been taxed at the general corporate rate. The DTC for these dividends is 15.0198%.

What Are Noneligible Dividends?

Small, privately held Canadian corporations (such as small businesses) can do the same, but pay a lower corporate tax rate, resulting in a less favourable tax credit of 9.0301%.

What's The “Gross Up” Rate?

As stated, dividends are distributed after a company has been taxed, and then you get taxed too!

To avoid this double taxation, the Income Tax Act uses the “gross up” mechanism. For eligible dividends, you’ll report 38% more income than what you actually received, whereas noneligible dividends “gross up” by 15% instead.

Double taxation isn’t ideal, and you may be asking yourself, “Wouldn’t I want to keep my taxable income lower? Why would I want a 38% increase rather than 15% instead?” That’s where the DTC comes into play.

What's The Dividend Tax Credit?

It’s a somewhat complicated solution to double taxation, but bear with us—the tax credit is relative to the “gross-up” percentage, so while you are technically reporting a higher income for eligible dividends, the DTC scales up to account for it and produce a more tax-efficient result.

How Do I Calculate The Dividend Tax Credit?

Ignoring the differences between provinces (for the sake of brevity), it’s quite simple to calculate the DTC. We’ll illustrate how, with a pair of hypothetical examples where you’ve earned $1,000, “gross up” the income, and apply the DTC while assuming a marginal tax rate of 30%.

The formula is INCOME x (1+“GROSS UP” RATE) x MARGINAL TAX RATE – (DTC x “GROSSED UP” INCOME)

Eligible Dividends

-

“Grossed up” reportable income: $1,000 x 1.38 = $1,380

-

Taxes owed per marginal rate: $1,380 x 0.30 = $414

-

DTC tax credit: $1,380 x 0.150198 = $207.27

-

Taxes owed after DTC credit: $414 - $207.27 = $206.73

-

After-tax returns: $1,000 – 206.73 = $793.27

Noneligible Dividends

-

“Grossed up” reportable income: $1,000 x 1.15 = $1,150

-

Taxes owed per marginal rate: $1,150 x 0.30 = $345

-

DTC tax credit: $1,150 x 0.090301 = $103.85

-

Taxes owed after DTC credit: $345 - $103.85 = $241.15

-

After-tax returns: $1,000 – $241.85 = $758.15

For the sake of transparency, if this were exclusively interest income (or foreign dividend income, which is treated similarly), the after-tax returns would be $700, and capital gains at the current inclusion rate of 50% would be $850 at the point of sale.

Dividends, however, generate income over time, and realized gains would be taxed even more favourably. If you choose to reinvest your distributions, well, the compounding effects can be incredibly lucrative over time.

Business Owners

Self-employed individuals may have their own unique situation, burdens, and opportunities when it comes to dividend income.

Dividends vs. Salary

Entrepreneurs can consider paying themselves dividends as opposed to a salary if they’re operating through a corporation. While this strategy may come with certain benefits (avoiding having to pay CPP contributions as both the employee and the employer), it also has drawbacks (fails to generate RRSP contribution room) and should be discussed in detail with your Family Wealth Advisor before doing so. For many, the most tax-efficient approach would be to pay yourself a mix of both forms of income.

Capital Dividends Account

In terms of triggering capital gains within a corporation, the Capital Dividend Account (CDA) can be a useful tool. As it stands, the CDA is a notional account for private corporations that allows them to pay tax-free capital dividends to shareholders.

The CDA balance is calculated by adding the non-taxable portion of capital gains or losses, capital dividends received from other corporations, and life insurance proceeds in excess of the policy’s adjusted cost basis.

Essentially, 50% of capital gains will be taxed, whereas the other half will go into the CDA and can be distributed to shareholders once a T2054 form has been prepared.

If Budget 2024's proposed changes to inclusion rates take effect, this tax-efficient method of accessing corporate funds could lose its appeal. Suddenly, only 33.33% of the gains will be eligible within the CDA, as the remainder will be subject to tax.

Bellwether Global Dividend Strategy

For income-oriented investors looking for a low-risk portfolio option that exhibits stability and long-term capital appreciation, the Bellwether Global Dividend Strategy could be a suitable choice.

As a tax-efficient investment vehicle with global diversification to deliver superior risk-adjusted returns, the Fund is designed to weather heightened market volatility by investing in profitable, proven growth companies. By prioritizing businesses that have a history of paying (and increasing) dividends to shareholders, we can achieve a lower turnover rate to minimize capital gains and further increase after-tax income.